Simulating Random Portfolios to Illustrate the Efficient Frontier in Python

A hands-on guide to modern portfolio theory: simulate thousands of random portfolios in Python to visualize the efficient frontier and identify the optimal Sharpe ratio allocation.

1) Background - The Efficient Frontier

Modern portfolio theory (MPT) is a mathematical framework for assembling a portfolio of assets such that risk-averse investors can construct portfolios to maximize expected return. This is based on a given level of market risk, emphasizing that higher risk is an inherent part of higher reward.

MPT uses weighted returns of equities to calculate a portfolio-wide return. Then it uses statistical measures such as variance (standard deviation) and correlation to determine 'risk' of a portfolio. It's important to note that for a portfolio comprised of 'n' assets you can't simply sum the standard deviation of each asset to calculate the total risk, but must also account for the correlation between assets.

Using MPT, one can calculate what is called the 'efficient frontier,' which is the set of 'optimal' portfolios that offer the highest expected return for a defined level of risk. In this post, we'll run thousands of portfolio simulations to highlight where the efficient frontier is, given a set of equities. The efficient frontier can also be calculated formulaically, but simulating and visualizing portfolio runs can help better illustrate what's going on.

If the above is all sounding like a lot, don't worry; it will become clearer as I step through the code example below!

2) Setting up a random portfolio of equities

First, let's grab some historical return data for a set of equities. We can then use this to generate random portfolios in our simulation:

import pandas as pd

from pandas_datareader import data as pdr

import fix_yahoo_finance as yf

import numpy as np

import datetime as dt

import matplotlib.pyplot as plt

plt.style.use('seaborn-colorblind')

%matplotlib inline

# Create our portfolio of equities

tickers = ['AAPL','FB', 'C', 'DIS']

# Download closing prices

data = pdr.get_data_yahoo(tickers, start="2018-01-01", end=dt.date.today())['Close']

# From the closing prices, calculate periodic returns

returns = data.pct_change()

# Preview the data

data.tail()

| Symbols | AAPL | FB | C | DIS |

|---|---|---|---|---|

| Date | ||||

| 2019-12-24 | 284.269989 | 205.119995 | 78.589996 | 145.289993 |

| 2019-12-26 | 289.910004 | 207.789993 | 79.830002 | 145.699997 |

| 2019-12-27 | 289.799988 | 208.100006 | 79.669998 | 145.750000 |

| 2019-12-30 | 291.519989 | 204.410004 | 79.510002 | 143.770004 |

| 2019-12-31 | 293.649994 | 205.250000 | 79.889999 | 144.630005 |

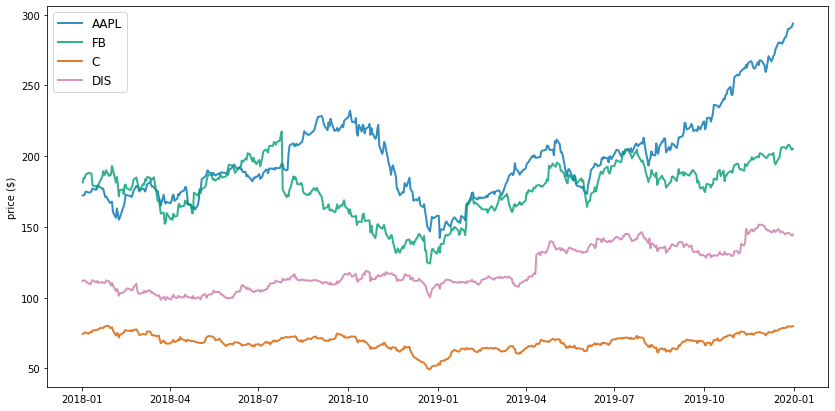

Next, just for general context into each stock's historical performance and to help sense check our numbers, we'll take a look at the price trends:

plt.figure(figsize=(14, 7))

for i in data.columns.values:

plt.plot(data.index, data[i], lw=2, alpha=0.8,label=i)

plt.legend(loc='upper left', fontsize=12)

plt.ylabel('price ($)')

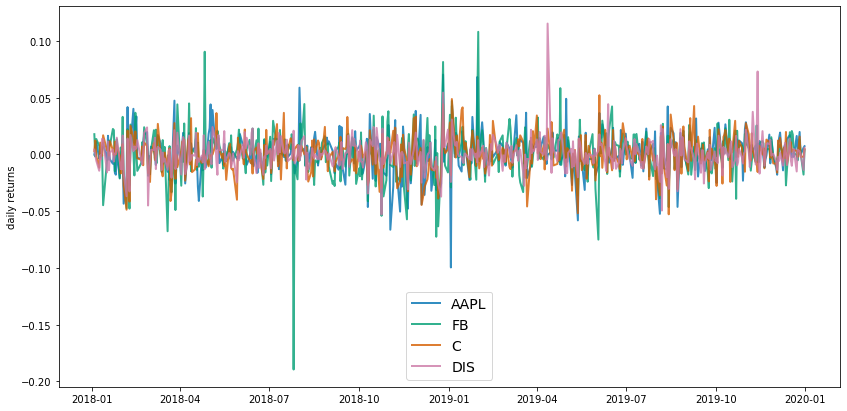

Plotting this using daily % change in return can help illustrate the stocks' volatility.

returns = data.pct_change()

plt.figure(figsize=(14, 7))

for i in returns.columns.values:

plt.plot(returns.index, returns[i], lw=2, alpha=0.8,label=i)

plt.legend(loc='lower center', fontsize=14)

plt.ylabel('daily returns')

This chart is a bit noisy with all of the equities plotted at once, but we can see Disney has a positive spike around April 2019, Facebook has one large negative spike along with some smaller positive/negative spikes, etc. Remember, in MPT the spikes = volatility which is then used as a proxy for risk.

3) Defining functions to simulate random portfolios

Now that we have the historical price data pulled, we'll define functions to assign random weights to each stock in the portfolio, then calculate the portfolio's overall annualized returns and annualized volatility.

We'll first create a function to calculate our portfolio returns and volatility:

# Define function to calculate returns, volatility

def portfolio_annualized_performance(weights, mean_returns, cov_matrix):

# Given the avg returns, weights of equities calc. the portfolio return

returns = np.sum(mean_returns*weights ) *252

# Standard deviation of portfolio (using dot product against covariance, weights)

# 252 trading days

std = np.sqrt(np.dot(weights.T, np.dot(cov_matrix, weights))) * np.sqrt(252)

return std, returns

Next we can create a function to generate random portfolios with random weights assigned to each equity:

def generate_random_portfolios(num_portfolios, mean_returns, cov_matrix, risk_free_rate):

# Initialize array of shape 3 x N to store our results,

# where N is the number of portfolios we're going to simulate

results = np.zeros((3,num_portfolios))

# Array to store the weights of each equity

weight_array = []

for i in range(num_portfolios):

# Randomly assign floats to our 4 equities

weights = np.random.random(4)

# Convert the randomized floats to percentages (summing to 100)

weights /= np.sum(weights)

# Add to our portfolio weight array

weight_array.append(weights)

# Pull the standard deviation, returns from our function above using

# the weights, mean returns generated in this function

portfolio_std_dev, portfolio_return = portfolio_annualized_performance(weights, mean_returns, cov_matrix)

# Store output

results[0,i] = portfolio_std_dev

results[1,i] = portfolio_return

# Sharpe ratio

results[2,i] = (portfolio_return - risk_free_rate) / portfolio_std_dev

return results, weight_array

Next, let's set up our final input variables, calculating the mean returns of each stock, as well as a covariance matrix to be used in our risk calculation below:

returns = data.pct_change()

mean_returns = returns.mean()

cov_matrix = returns.cov()

# Number of portfolios to simulate

num_portfolios = 10000

# Risk free rate (used for Sharpe ratio below)

# anchored on treasury bond rates

risk_free_rate = 0.018

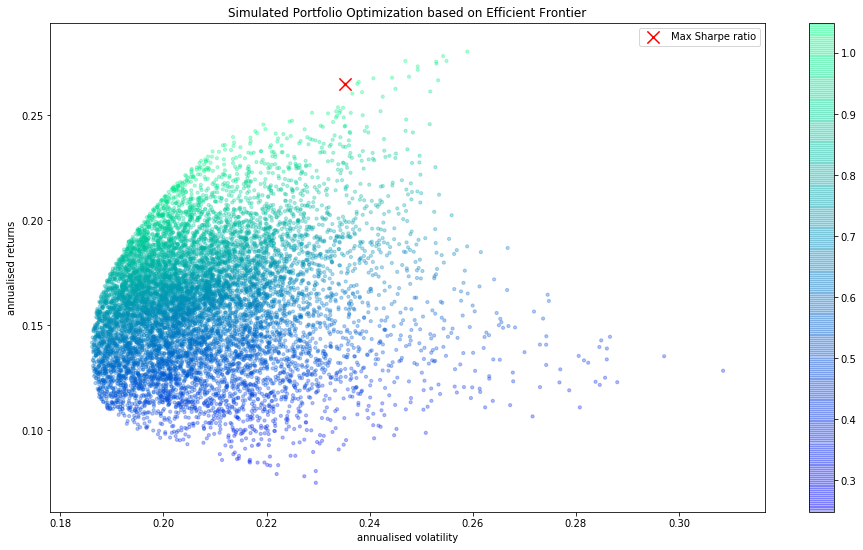

4) Simulating portfolio returns/variance, visualizing the efficient frontier

Finally, we can toss everything together in one final function below. The below function is generating a random portfolio, obtaining the returns, volatility, and weights. We'll also go ahead and add an annotation showing the maximum Sharpe ratio (the average return earned in excess of the risk-free rate per unit of volatility or total risk). In general, a higher Sharpe ratio is better.

All of the randomly generated portfolios will be plotted with a color map applied to them based on the Sharpe ratio. The more green, the higher the Sharpe ratio.

For the 'optimal' portfolio with the highest Sharpe ratio (highest returns relative to risk), we'll also print the % allocation across the portfolio:

def display_simulated_portfolios(mean_returns, cov_matrix, num_portfolios, risk_free_rate):

# pull results, weights from random portfolios

results, weights = generate_random_portfolios(num_portfolios,mean_returns, cov_matrix, risk_free_rate)

# pull the max portfolio Sharpe ratio (3rd element in results array from

# generate_random_portfolios function)

max_sharpe_idx = np.argmax(results[2])

# pull the associated standard deviation, annualized return w/ the max Sharpe ratio

stdev_portfolio, returns_portfolio = results[0,max_sharpe_idx], results[1,max_sharpe_idx]

# pull the allocation associated with max Sharpe ratio

max_sharpe_allocation = pd.DataFrame(weights[max_sharpe_idx],index=data.columns,columns=['allocation'])

max_sharpe_allocation.allocation = [round(i*100,2)for i in max_sharpe_allocation.allocation]

max_sharpe_allocation = max_sharpe_allocation.T

print("-"*100)

print("Portfolio at maximum Sharpe Ratio

")

print("--Returns, volatility--

")

print("Annualized Return:", round(returns_portfolio,2))

print("Annualized Volatility:", round(stdev_portfolio,2))

print("

")

print("--Allocation at max Sharpe ratio--

")

print(max_sharpe_allocation)

print("-"*100)

plt.figure(figsize=(16, 9))

# x = volatility, y = annualized return, color mapping = sharpe ratio

plt.scatter(results[0,:],results[1,:],c=results[2,:], cmap='winter', marker='o', s=10, alpha=0.3)

plt.colorbar()

# Mark the portfolio w/ max Sharpe ratio

plt.scatter(stdev_portfolio, returns_portfolio, marker='x',color='r',s=150, label='Max Sharpe ratio')

plt.title('Simulated portfolios illustrating efficient frontier')

plt.xlabel('annualized volatility')

plt.ylabel('annualized returns')

plt.legend(labelspacing=1.2)

display_simulated_portfolios(mean_returns, cov_matrix, num_portfolios, risk_free_rate)